Introduction

This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader context of the international hospitality industry as well as of Greek tourism and Greek socio-economic developments.

Tourism sector recovery

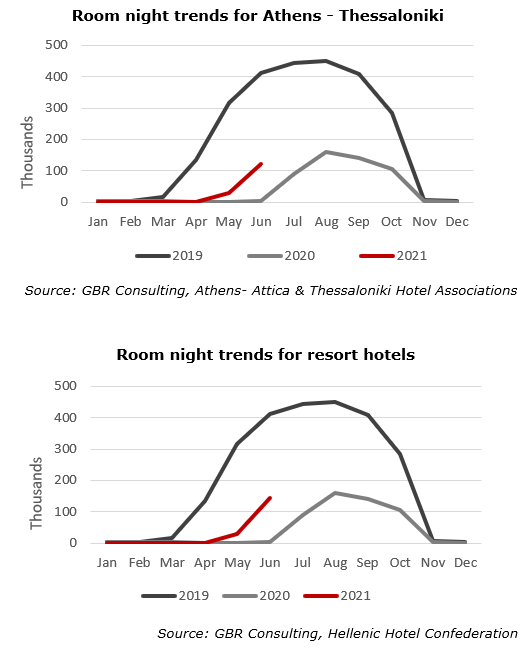

- After the opening of tourism in mid May 2021, the tourism industry slowly commenced its recovery. International arrivals at Greece’s main airports in June 2021 did not exceed a level of 35% of 2019.

- This is in line with our room night trend analysis, which shows that Greek hotels reached a level of 38% in June 2021 compared to June 2019: 43% in Athens & Thessaloniki, 35% at resort hotels.

- In Athens 87% of the room supply was in operation in June with increased demand.

Room revenue in June 2021 achieved a level of 39% of the same month in 2019.

- In Thessaloniki about 88% of the rooms were operational in June, while demand picked up.

Room revenue in June 2021 reached a level of 44% of the performance in June 2019.

- About 72% of the resort hotels participating in our monthly performance survey were in operation in June 2021, reaching total revenues of 48% of the level of June 2019.

Higher average spend at resort hotels

- Our data of June 2021 also shows that the Total Revenue per Occupied room at resort hotels is significantly higher than June 2020 – with very low demand – but also compared to June 2019.

- This could indicate that Greece is attracting a higher profile customer, who is willing to spend more, possibly supported by available excess savings accumulated during the pandemic.

Promising outlook for H2 2021 but it is fragile

- Air traffic shows significant accelerations in recent weeks. Greek hoteliers are optimistic for the coming months, but remain cautious as demand is fragile with fears of the spreading of the Delta variant, which is much more transmissible than the previous leading variant.

- Significant pent-up demand supported by considerable excess savings certainly will drive tourism, but governments continuously implement new restrictions for incoming tourists, but also for returning tourists. Every country determines its own travel policies so no harmonized EU set of travel rules and restrictions are in place.

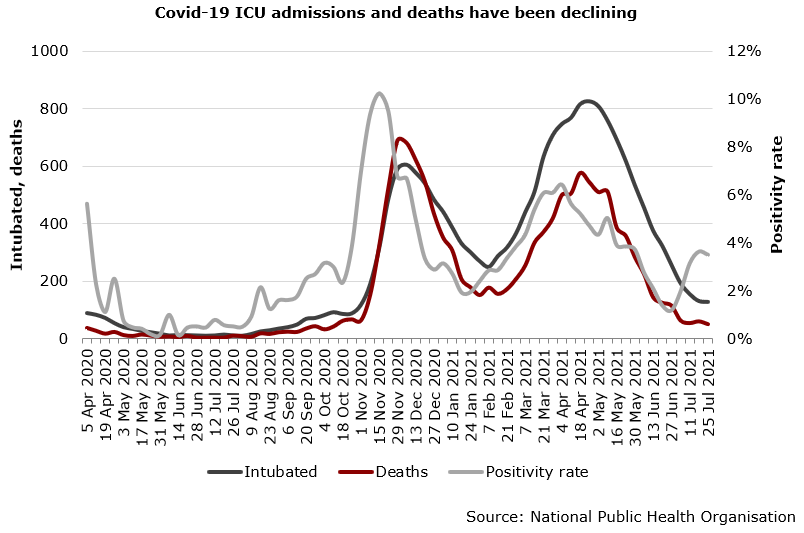

- As depicted in the graph below, Covid-19 related ICU admissions and deaths in Greece have declined during the last 3 months due to the vaccination program. However, the positivity rate has also increased since June. New Covid-19 infections are mainly seen among young people, while also the age group of 40 – 64 shows increasing infections.

- Currently, 29 July 2021, according to Our World in Data 48% of the Greek population has been fully vaccinated, while 54% has at least one vaccine dose. This means that Greece is behind its competitors: Spain (57% fully vaccinated, 67% at least one vaccine dose), Portugal (54% fully vaccinated, 68% at least one vaccine dose), Italy (50% fully vaccinated, 62% at least one vaccine dose). Turkey, however, is far behind with 30% of population fully vaccinated and 48% with at least one vaccine dose.

Greek economy: stronger-than-expected H1 will lift recovery this year

- The coronavirus pandemic was a massive drag on the Greek economy last year, with GDP falling 7.8%. National accounts showed that GDP outperformed in Q1 this year, rising 4.4% q-o-q despite lockdown measures having been reimposed. Investment expanded by 3.0% q-o-q and net trade recovered further, but private consumption continued to suffer due to the prolonged restrictions that halted spending.

- Oxford Economics expects that GDP will expand marginally in Q2. Available hard data show mixed signs with industrial production dropping 5.1 % m-o-m in May, offsetting April 4.4% rise, but retail sales up 2.3% m-o-m in April. In addition, sentiment data for June saw confidence fading. Despite the EC’s Economic Sentiment Indicator improving marginally, all components apart from services deteriorated, reversing the upward trend seen in recent months. Jobs data suggest fragility in the labour market, with the number of unemployed rising more than the number employed in April.

- Also tourism activity remained weak during Q2 2021 with travel receipts in April and May at levels of 8% and 11% of the respective month in 2019 according to data released by the Bank of Greece.

- Oxford Economics forecasts a growth of 5.7% in 2021 as activity is expected to recover gradually during the rest of the year with the following key drivers: increased household spending, rise in investments supported by the Next Generation EU funding, recovering exports with improved travel activity.

Transactions

- At the beginning of July 2021 it was announced that Hotel Investment Partners (HIP) signed an agreement to acquire the Elounda Blu hotel from the Ledra Hotels & Villas group. Elounda Blu is a 4-star hotel with 183 rooms and is located in Elounda, Crete. According to reports, more than € 6 million will be invested in the upgrading and rebranding the hotel to an international 5-star branded resort.

- The American real estate company Hines acquired the Out of the Blue Capsis Elite Resort which is located in Agia Pelagia of Heraklion, Crete. Hines set the highest price in an auction held on Thursday, July 15 as it offered about € 125 million (~ € 255,000 per room), while the bids of a consortium of Prodea, Invel & Yoda Investments (€ 87 million) and Piraeus Financial (€ 50 million) were significantly lower. The Out of the Blue Capsis Elite Resort is a 5-star hotel with 490 rooms.

- A competition organized by the Hellenic Republic Asset Development Fund (HRADF) and by the Hellenic Public Properties Company (HPPC) for the right of surface for 99 years of the Xenia Hotel and the “Kakavos” and “Agioi Anargyroi” thermal springs in Kythnos has been completed. Greek media mention that Israeli businessman Avraham Ravid has offered € 2.8 million, but contracts need to be finalized in the coming period.

Greek hotel brand landscape in 2021

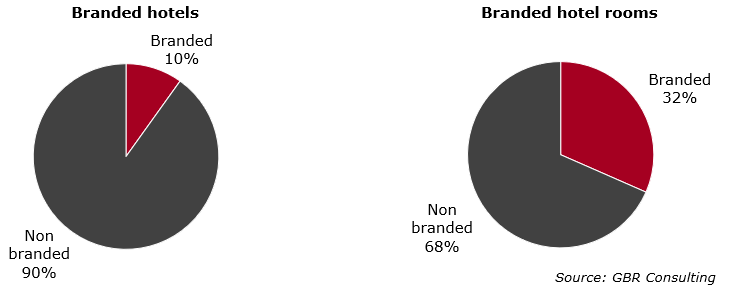

- GBR Consulting has completed a new research on the hotel brand landscape in Greece. The analysis shows that currently 10% of all hotels and 32% of all hotel rooms are branded, which means that a hotel is part of an international brand with hotels in more than one country, a national brand with a presence in various geographic regions within Greece, a local brand with a presence of more than 1 hotel in only one geographic area and / or a consortium, covering hotels that are part of a marketing partnership.

- The brand penetration rate of 10% mentioned above represent 1,022 hotels who carry 1,479 brands. Many hotels carry multiple brands, even up to 6 brands. The marketing consortia have the largest market share with 45%, followed by international and national brands with 19% each and local brands with 17%.

- A 198 distinct brands of all mentioned types have a presence in Greece currently, of which 63 are international.

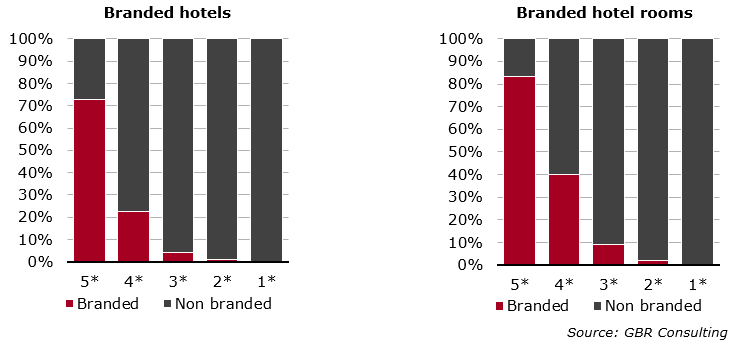

- In the 5-star sector about 73% of the hotels and 83% of the hotel rooms are branded, while in the 4-star category these rates are 23% and 40% respectively.

Hotel brands are on the rise

- Compared to 2016, the number of branded hotels increased by 65% and branded hotel rooms by 59%. The overall brand penetration rate at hotels in 2016 was 6% compared to 10% in 2021, while penetration rate of hotel rooms was 21% in 2016 compared to 32% in 2021.

- In 2016 we had 137 distinct hotel brands registered in our database, compared to 198 in 2021, an increase of 45%

- Internationally branded hotels showed the largest growth of 95% comparing 2016 to 2021. The 5-star sector increased their brand penetration from 53% in 2016 to 73% in 2021 in terms of hotels and from 65% in 2016 to 83% in 2021 in terms of hotels rooms.

- Some of the international brands which entered the Greek market during the last 5 years are brands of Marriott International (entered with Autograph Collection Hotels, Marriott Hotels and Moxy), Brown Hotels, Cook & Cook's Club (both former Thomas Cook), Hilton Worldwide (entered with Curio Collection), Four Seasons, Wyndham Hotel Group (entered with Dolce Hotels & Resorts, Ramada, Wyndham Grand and Wyndham Hotels & Resorts), Accor (entered with Angsana, Ibis Styles and MGallery), Labranda Hotels & Resorts (FTI), OKU Hotels and Pacha Group.

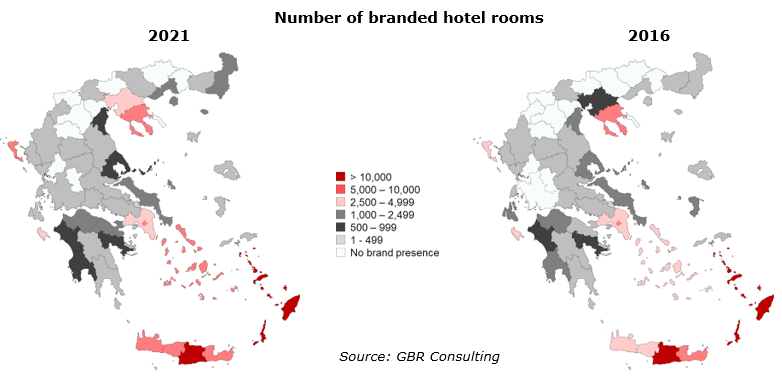

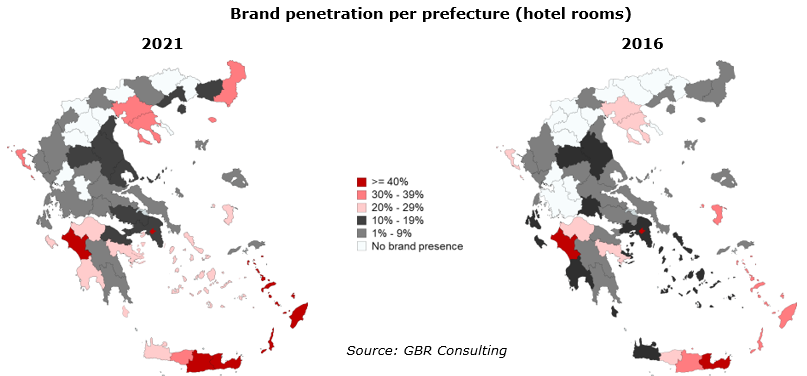

Hotel brand landscape per prefecture

- In 2016 Athens, Lassithi (Crete) and Ilia (west Peloponnese) were the only regions with a brand penetration of more than 40% in terms of hotel rooms. In 2021 the Dodecanese and Iraklio (Crete) were added to this category.

- The prefecture with the most branded hotel rooms by far is the Dodecanese with nearly 40,000 rooms, followed at a distance by Iraklio in Crete with nearly 19,000 rooms and Halkidiki with about 9,500 rooms categorized below in a bracket of between 5,000 – 10,000 hotel rooms.

|