Introduction

This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader context of the international hospitality industry as well as of Greek tourism and Greek socio-economic developments.

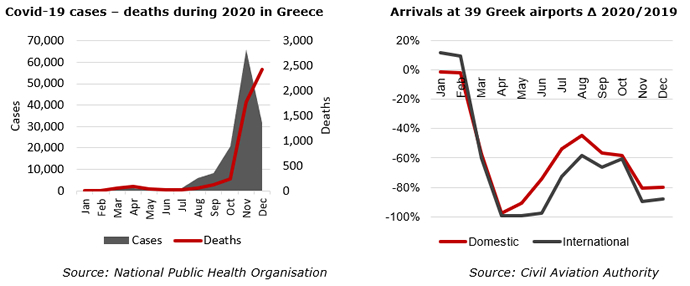

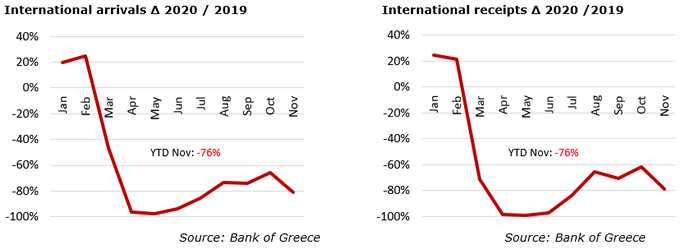

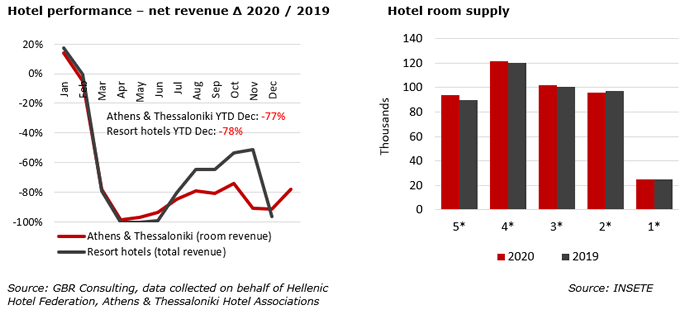

The year 2020 in 6 graphs

Gloomy outlook for H1 2021 and rebound in H2 2021

- At the midst of

- high levels of new cases worldwide,

- the spreading of new variants of the virus (U.K., South Africa and Brazil),

- extended and in some cases stricter lock downs in many countries,

- the slow start of the vaccination process,

- delays of vaccine deliveries from AstraZeneca and Pfizer,

the outlook for the tourism sector and the economy, especially for those countries with high dependence on tourism, is currently highly uncertain.

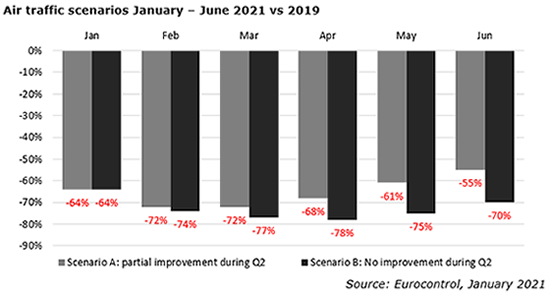

- Eurocontrol released on January 28th, 2020 new traffic scenarios for the period up to 2021. Air traffic throughout Europe was approximately 64% down in January 2021 y-o-y and the situation is quickly deteriorating as February and March will be exceptionally low across the network. Even April is expected to perform very poorly according to Eurocontrol with only a limited pick-up for the Easter period. Flights are projected to be around 25 – 30% of normal.

- In scenario A as displayed in the chart below, it is assumed that the epidemiological European situation will improve after March and that the most vulnerable citizens across Europe will have been vaccinated (despite delays) facilitating the partial relaxation of national travel restriction measures during Q2. That means that non-essential air travel will become more accessible during Q2 followed by a larger recovery in the summer period. In scenario A traffic levels will be at -55% of 2019 by June 2021.

- However, Eurocontrol does not find scenario B unreasonable, where the epidemiological situation will be improved by Q2, but many states may potentially choose not to relax their national travel restrictions, which will severely curtail demand and any possibility for air travel to improve until the summer period at the very earliest.

- In Greece market players are anticipating a strong rebound of travel activity in the second half of this year. SETE, the Greek Tourism Confederation, predicts based on current data that the Greek tourism sector could achieve 50% of the tourism revenue of 2019.

- As analysed in our newsletter of 2020 Q3, the international business segment is hardest hit and is expected to recover to 2019 levels only after 2024. This has a significant impact on the tourism sector as business travellers are high spenders. For airlines the business segment represents a small share of the passengers, but a very large share of the profits. This development could have an impact on fares.

- When business does return, it is likely that its form has changed. The MICE industry has already adapted with hybrid / digital solutions and is expected to replace partly the face-to-face meetings that will also return in the long run.

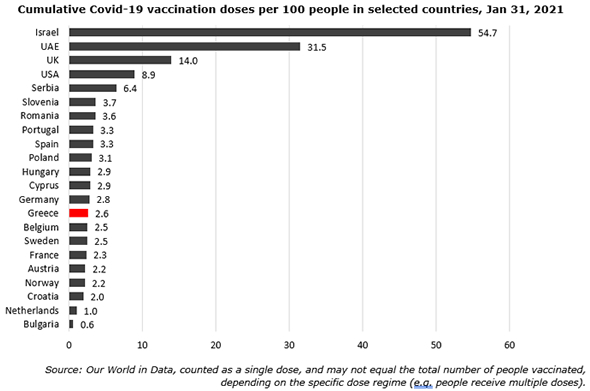

Vaccine rollout crucial

- Greece launched its Covid-19 vaccine rollout, “Eleftheria” at the end of December 2020. The first priority group includes health and social care professionals and nursing home residents and staff, employees at chronic care facilities and rehabilitation centers and staff working in critical government functions. The second priority group is expected to start the vaccination process in February and will include people aged 70 and over regardless of medical history with priority given to older individuals and to those with medical issues.

- Equally important is the roll out of vaccinations in Greece’s major source markets such as Germany, United Kingdom, Italy, France, The Netherlands, Bulgaria and United States, but also on a worldwide scale as new mutations will keep on developing and spreading if for instance some parts of the world will stay behind.

- Therefore, the World Health Organisation stressed that available vaccines should be equally distributed in all countries to protect effectively. A global initiative was launched, COVAX, to ensure that poorer countries would also have fair access to vaccines for the coronavirus and to avoid vaccine nationalism. The program secured financial support from the EU, from countries such as Canada, France, Germany and charitable institutions. Billions of doses have been secured, but none has been delivered to the 92 countries that cannot afford to buy vaccines on their own.

- Meanwhile, because rich countries seem to look inward, Russia's Sputnik V and China's Sinovac has been taken up through deals with several countries such as Turkey, Indonesia, Brazil, Belarus, Argentina and Thailand, despite questions around its efficacy.

Economy

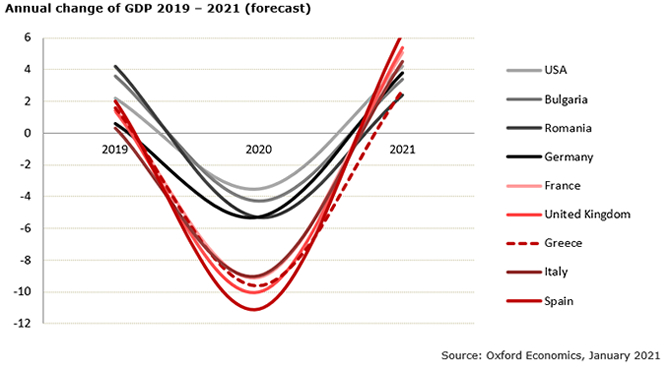

- In general, weaker economic growth for Q1 2021 is anticipated with hopes for a stronger rebound in Q2 2021 and Q3 2021, once the most vulnerable groups are vaccinated and restrictions can be rolled back.

- Most countries started their vaccination programme with healthcare workers, frontline workers, elderly and people with severe health conditions. While near-term Covid-19 risks are tilted to the downside, gradual vaccine diffusion, loosening of social distancing restrictions, supportive monetary and fiscal policies and warmer weather should ensure stronger economic activity and employment from the spring onwards.

- For Greece it is estimated that GDP fell 9.6% in 2020 and will rebound to a growth of just 2.7% in 2021 according to Oxford economics given the worsening health situation and lockdowns heavily weighing on activity, while the course of the tourism sector remains uncertain. For 2022 analysts expect a robust growth.

- Recent data shows that Covid containment measures at the end of 2020 will result in a double-dip recession in Italy. Oxford economics expects output to have fallen again in Q4 2020. This weakness is set to continue in early 2021. For Q1 2021 the analysts expect GDP to be flat, but for 2021 as whole a GDP growth of 4.5% is forecasted. A return to the pre-crisis GDP levels is not expected until end-2022.

- The roll-out of vaccinations in France has been slow compared with other EU countries, raising fears that enough inoculation to allow economic activity to normalize will not be reached until after the summer. In this context, GDP growth is expected to be 5.1% in 2021 after an estimated 9.1% contraction in 2020.

- While latest data suggest that economic activity in Spain was not as weak as previously expected in Q4 2020, the extension of restrictions due to the renewed deterioration in the health situation will translate into lower growth in Q1 2021. It is projected that GDP contracted by 11.1% in 2020 and will bounce back by 6.3% in 2021.

Planning for the future

Transactions and main developments in the Greek tourism sector

- In November 2020 it was announced that Cretan Investments Group (CIG) Hellas acquired its first hotel, the 119-room Iti AKS Minoa Palace. The hotel located in Heraklion, Crete will be renovated in two phases (during the winter of 2020 / 2021 and 2021 / 2022) and is planned to reopen in April 2021 as the Sentido Unique Blue Resort. No further transaction details have been released.

- On November 27th, 2020 Lamda Development and TEMES S.A. announced a strategic agreement for the joint development of two state of the art, luxury hotels and residential complexes on the coastal front of Hellinikon during the first five-year phase of the project. The strategic agreement envisages, the development of a 5-star hotel of distinct architecture at the Agios Kosmas marina, as well as a second beach front 5-star luxury hotel along the coastal front. Both hotels will be accompanied by branded residences and the total investment is estimated at € 300 million.

- In addition to these two luxury hotels, Mohegan – GEK Terna will start construction of the Integrated Resort & Casino as soon as licenses are issued. Once that process has been finalised, the project should be completed in 3 years. Finally, a 4-star (superior) hotel is planned near Vouliagmenis Ave. next to the business centre offering 500 rooms.

Most elements of the project including the 4 hotels are scheduled for opening during 2025 and will bring about 2,500 new rooms to the Attica hotel market.

- The Sarantis family, who founded and manages the dairy industry TYRAS (HELLENIC DAIRIES SA), acquired the 5-star Ananti City Resort, located on the hill of Longaki, at a distance of 3.5 km from the city center of Trikala. Ananti Resort has 18 rooms and suites, a rooftop bar / restaurant, spa & wellness centre, indoor heated and outdoor pool and underground parking.

- Finally, Everty, the real estate arm of investment group YNV announced in December 2020 that it is planning to invest € 100 million in the Greek property market by acquiring assets in the office market, hospitality and residential sectors with an emphasis on luxury holiday villas.

|