Introduction

This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader context of the international hospitality industry as well as of Greek tourism and Greek socio-economic developments.

Hotels are suffering amid a dramatic drop in demand

- The covid-19 crisis hit hard the Greek hospitality sector as travel for business and leisure dried up.

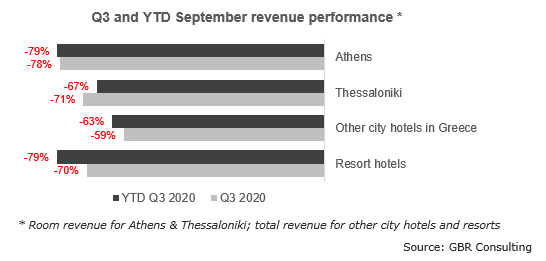

- Our analysis shows that through the end of September 2020, room revenue of hotels in Athens and Thessaloniki dropped y-o-y by 79% and 67% respectively.

- Total revenue of city hotels located elsewhere declined by 63% y-o-y YTD Q3 2020, while resort hotels registered a staggering drop of 79% y-o-y during the same period

- These figures also reflect the fact that after the spring lockdown many hotels remained closed or reopened only to close again. During September 77% of the room supply in Athens and 88% of hotel rooms in Thessaloniki were in operation.

- In September, usually the peak month of the year, RevPAR in Athens and Thessaloniki reached € 25, a drop of 79% and 65% y-o-y respectively.

Very low demand during Q3 2020

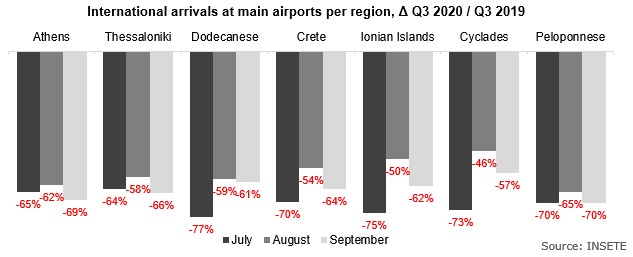

- Despite the country’s success in controlling the first wave of covid-19 and the projected image as a safe destination where hoteliers took all necessary safety measures, appetite for travelling to Greece remained low. During Q3 2020, international arrivals at Greece’s main airports stood at 3.9 million passengers, a decline of 64% from the 10.8 million during the same period in 2019. On average, July declined by 71% y-o-y, August by 57% y-o-y and September by 64% y-o-y.

- Analysis of traffic data from all airports in major regions followed a similar trend.

- Domestic arrivals at the main Greek airports dropped by 53% y-o-y during Q3 2020, bringing the YTD decline to 58%. During the same period road arrivals decreased by 89% and 76% respectively.

- The Bank of Greece in its monthly release of developments in the balance of travel services showed that as of the end of August 2020 travel receipts YTD declined to just € 2.7 billion from € 12.9 billion in 2019, a drop of 79.7% y-o-y.

- During the same period the number of inbound travellers declined by 17 million to just 4.8 million. Border restrictions were the main cause for an even sharper decline in the number of travellers from the United States and Russia which reached 88% and 94% respectively. Arrivals from Germany declined by 72.7% y-o-y up to August.

Outlook for air travel and implications for tourism in Greece

- In October 2020, IATA and Tourism Economics published their research and expectations of what lies ahead. Tourism Economics is an Oxford Economics specialty research outfit and IATA (International Air Transport Association) represents some 290 airlines comprising 82% of global air traffic.

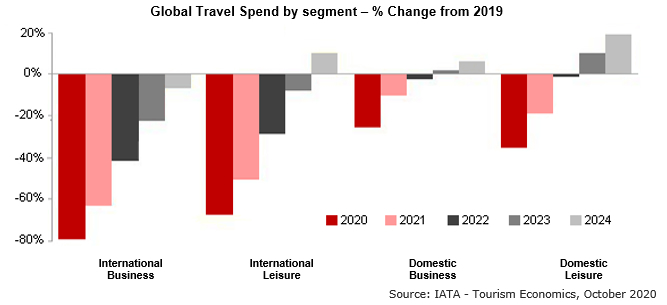

- They concluded that the international business segment is hardest hit and will recover to 2019 levels only after 2024.

- Domestic business travel was the least affected segment in 2020, and domestic leisure travel will be the fastest to recover, reaching 2019 levels in 2022.

- In this respect, the primary leisure destinations in Greece, such as Crete, the Dodecanese, the Ionian Islands and the Cyclades will suffer for longer because of their high dependency on foreign tourists. In 2019 the share of overnight stays of Greeks at hotels in Crete, Dodecanese, Ionian Islands and the Cyclades was 4%, 4%, 7% and 15% respectively.

- International leisure travel is projected to recover in 2024 on a global level, meaning that until then the excess supply of hotel accommodation will vie for a piece of a much smaller pie.

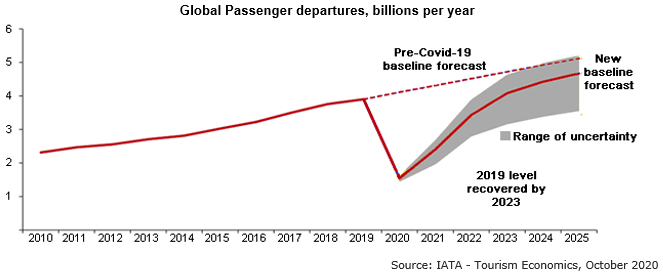

- The IATA and Tourism Economics research includes the air passenger departures forecast shown below, as seen before and after covid-19.

- Its key observations are that the baseline scenario reaches the 2019 level in 2023, but even by 2025 traffic remains well below the pre-covid-19 forecast. At the same time risks remain tilted to the downside.

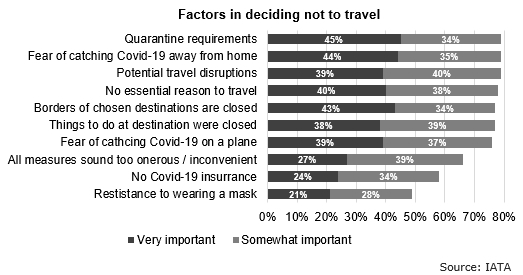

- In its analysis of which are the most important factors in deciding not to travel, IATA found that quarantine requirements, fear of catching Covid-19 away from home and the potential for travel disruptions such as cancelled flights weigh most heavily:

Covid-19

- Currently new Covid-19 cases are soaring in Europe and new measures and lockdowns are coming into force.

- In Greece new cases are rapidly increasing, and currently 7 regional units in the north (Thessaloniki, Serres, Rodopi, Larissa, Kozani, Kastoria and Ioannina) are classified at “Level 4”, the highest risk rating requiring strict measures to be imposed. Attica is rated at ”Level 3”, indicating high risk and increased monitoring.

- So far Greece registered 35,510 cases and 615 deaths.

Impact on Greek economy

- The economic impact of the coronavirus pandemic will lead to a sharp contraction of Greek GDP in 2020. Economic activity fell by a staggering 14.1% q/q in Q2. Oxford Economics forecasts that GDP will decline by 8.3% y-o-y in 2020 before rebounding to growth of just over 7% in 2021.

- However, risks remain tilted to the downside given the subdued recovery in tourism and the recent rise in new cases of coronavirus in Greece and across Europe as outlined above.

- The fiscal flexibility granted to the Greek government by the EU has provided some fiscal space and the comprehensive package of fiscal measures financed both by the government and the EU will soften the blow from the crisis. The package included an immediate fiscal impulse, tax and social contribution deferrals and other liquidity and guarantee measures. Together with the utilisation of European funds, the total cost of the measures should reach € 24 billion (14% of GDP). The crisis will inevitably lead to a large fiscal deficit this year (which is currently forecasted at around 7% of GDP), while public debt is seen rising from 177% of GDP to around 190% in 2020.

Main developments and transactions

- In August 2020 it was announced that Lmey Investments AG acquired the remaining 50% of Westfort Capital (formerly Thomas Cook Hotel Investments). Westfort was established in May 2018. The newly built Casa Cook Kos is part of the portfolio and has been rebranded as Oku Kos. Westfort interests in Greece include the Sunwing Kalithea Beach Resort in Rhodes, the Sunwing Makrigialos Resort in Crete and a plot of land in Kos.

- At the end of September, the Sani Ikos Group announced that it will develop a second Ikos Resort on the island of Corfu, the Ikos Odisia, following the 5-star 403-room Ikos Dassia, which opened in 2018.

- The Radisson Hotel Group is planning for its third hotel after the Radisson Blu Park in Athens and the Radisson Blu Beach Resort in Crete. The Fais Group will develop the new 5-star 102-room hotel in Kamari on the island of Santorini and will carry the name Radisson Blu Zaffron Resort. The investment is estimated at € 15 million and the resort is scheduled to open in the second quarter of 2021.

- Mid October the Hellenic Gaming Commission named the consortium of Mohegan Gaming & Entertainment (MGE) and Greek construction company GEK TERNA preferred bidder for the concession of a casino license in the Hellenikon project. The consortium’s € 150 million bid for the sole 30-year casino license was five times the minimum set by the HGC. The development cost of its “Inspire Athens” complex has been estimated at around € 1 billion by the consortium.

- In July media reported that the Astir Palace Resort sold its first two villas for € 40 million each. The buyer is said to be a Greek shipowner and has taken an option for two more units

New hotel openings in Athens

- The hotel properties that had been in the development pipeline opened in a market with very weak demand:

- On September 1st Lampsa Hellenic Hotels inaugurated the 177-room 5-star Athens Capital Hotel – MGallery Collection at Syntagma Sq. It is the first MGallery (an Accor brand) in Greece. The conversion of the former ATEBank HQ back to a hotel required an investment of € 22 million.

- Global lifestyle hospitality brand Selina opened the Selina Theatrou Athens in August. It offers community rooms, shared kitchen, private rooms, restaurant, bar and events & activities.

- In September the new 4-star Athens 1890 Boutique hotel opened offering 14 rooms. The hotel is located at Agia Irini Sq in the centre of Athens.

- At the former Canadian Embassy in Kolonaki, a property of Briq Properties, the second hotel of the Modernist chain opened in September after a renovation of € 1.8 million by the lessee. The 4-star hotel offers 35 rooms.

- In August the Asomaton opened at a property owned by Treppidis Investments and is part of the Oniro Hotels Group. The 19-room property is located in Thissio and is managed by Celetrum.

- As from August the second hotel of Brown Hotels is in operation under the name The Dave Red. The 3-star hotel offers 87 rooms and is located at Veranzerou St behind Omonia Sq, in a building used previously by the Communist Party as offices.

- In June the 4-star Gem Society Boutique Hotel & Spa opened in the centre of Athens, offering 35 rooms and suites, a restaurant and spa.

- The 27-key, 3-star Royalty hotel opened this summer located near Monastiraki Square.

- AUM Group, a real estate development company, opened the Shila Athens in Kolonaki at a 1920s residence, a small unit with 6 suites. The company is planning for a second unit in Monastiraki at a former textile factory.

- Many accommodation projects are still in the pipeline for Athens and will further expand supply in the coming years. At the same time market rumors persist about projects slated for hotel development changing to other uses and sharing economy units being converted back to regular apartments for rent.

- Finally, the Greek Environment and Energy Ministry has approved the relocation of the Regency Casino Mont Parnes to the Dilaveri estate of the Laskaridis family in the municipality of Maroussi in the north of Athens. Besides the casino the property will also house a 5-star hotel, restaurants, conference and event space and underground parking.

|